Showing posts with label NOTIFICATIONS. Show all posts

Showing posts with label NOTIFICATIONS. Show all posts

Wednesday, 16 July 2014

Wednesday, 2 July 2014

Webcasts for IPCC by ICAI

| Subject | Link |

| Paper 2 – IPCC (Updates related to Companies Act , 2013 ) | |

| Paper 6 – IPCC ( Updates of Companies Act 2013 related to Auditing ) | |

| Paper 3 – IPCC ( Financial Planning And Analysis ) |

Timings : 3pm to 5pm

Monday, 23 June 2014

Syllabus For Nov 2014 IPCC Examinations

Revision of syllabus of Group – I

Paper- 4 - Taxation – Part – II

and

Group – II

Paper – 7 - Section A: Information Technology

of Intermediate (IPC) Course

PART II – INDIRECT TAXES (50 MARKS)

Objective:

To develop an understanding of the basic concepts of the different types of indirect taxes and to

acquire the ability to analyse the significant provisions of service tax.

1. Introduction to excise duty, customs duty, central sales tax and VAT – Constitutional

aspects, Basic concepts relating to levy, taxable event and related provisions

2. Significant provisions of service tax

(i). Constitutional Aspects

(ii) Basic Concepts and General Principles

(iii) Charge of service tax including negative list of services

(iv) Point of taxation of services

(v) Exemptions and Abatements

(vi) Valuation of taxable services

(vii) Invoicing for taxable services

(viii) Payment of service tax

(ix) Registration

(x) Furnishing of returns

(xi) CENVAT Credit [Rule 1 -9 of CENVAT Credit Rules, 2004]

Note – If new legislations are enacted in place of the existing legislations the syllabus will

accordingly include the corresponding provisions of such new legislations in place of the existing

legislations with effect from the date to be notified by the Institute. Students shall not be examined

with reference to any particular State VAT Law.

Intermediate (IPC), Group-II, Paper-7A: Information Technology

Paper - 7A: Information Technology (50 Marks)

Level of Knowledge: Working Knowledge

Objective: “To develop understanding of Information Technology as a key enabler and facilitator of

implementing Information Systems in enterprises and their impact on business processes and controls”.

Contents :

1. Business Process Management & IT

· Introduction to various Business processes – Accounting, Finances, Sale, Purchase etc.

· Business Process Automation – Benefits & Risks

· Approach to mapping systems : Entity Diagrams, Data Flow Diagrams, Systems Flow

diagrams, Decision trees/tables,

· Accounting systems vs. Value chain automation, Information as a business asset

· Impact of IT on business processes, Business Risks of failure of IT

· Business Process Re-engineering

2. Information Systems and IT Fundamentals

· Understand importance of IT in business and relevance to Audit with case studies.

· Understand working of computers and networks in business process automation from

business information perspective

· Concepts of Computing (Definition provided by ACM/IEEE and overview of related

terminologies)

· Overview of IS Layers – Applications, DBMS, systems software, hardware, networks &

links and people

· Overview of Information Systems life cycle and key phases

· Computing Technologies & Hardware – Servers, end points, popular computing

architectures, emerging computing architectures & delivery models – example: SaaS, Cloud

Computing, Mobile computing, etc.

· Example: Overview of latest devices/technologies – i5, Bluetooth, Tablet, Wi-Fi, Android,

Touchpad, iPad, iPod, Laptop, Notebook, Smartphone, Ultra- Mobile PC etc.)

3. Telecommunication and Networks

· Fundamentals of telecommunication

· Components and functions of Telecommunication Systems

· Data networks – types of architecture, LAN, WAN, Wireless, private and public

networks etc.

· Overview of computing architectures – centralised, de-centralised, mainframe, clientserver,

thin-thick client etc.

· Network Fundamentals – Components, Standards and protocols, Network risks &

controls – VPN, Encryption, Secure protocols,

· Network administration and management – concepts and issues

· How information systems are facilitated through telecommunications.

· How Internet works, Internet architecture, key concepts, risks and controls

· e-Commerce and M-commerce technologies

4. Business Information Systems

· Information Systems and their role in businesses

· IT as a business enabler & driver – ERP, Core Banking System, CRM, SCM, HRMS,

Payment Mechanisms

· The relationship between organisations, information systems and business processes

· Accounting Information Systems and linkages to Operational systems

· Business Reporting, MIS & IT

· Organisation Roles & responsibilities and table or authorities, importance of access

controls, privilege controls

· Specialised systems - MIS, DSS, Business Intelligence, Expert Systems, Artificial

Intelligence, Knowledge Management systems etc.

5. Business process automation through Application software

· Business Applications – overview and types

· Business Process Automation, relevant controls and information systems

· Information Processing & Delivery channels and their role in Information Systems

· Key types of Application Controls and their need

· Emerging concepts – Virtualisation, Grid Computing, Cloud delivery model

For Official Notification :

Click Here

Applicability of Companies Act 2013

(Paper 2 - Law)

Applicability of Companies Act 2013

(Paper 2 - Law)

As students may be aware that The Companies Act 2013 has been notified in the Official Gazette on 30th August, 2013 stating that different dates may be appointed for enforcement of different provisions of this Act through notification of the Central Government in this regard.

Having regard to the above development, the Council at its 330th meeting revised the syllabus in a limited manner in the following papers of Intermediate (IPC) as per Annexure I .

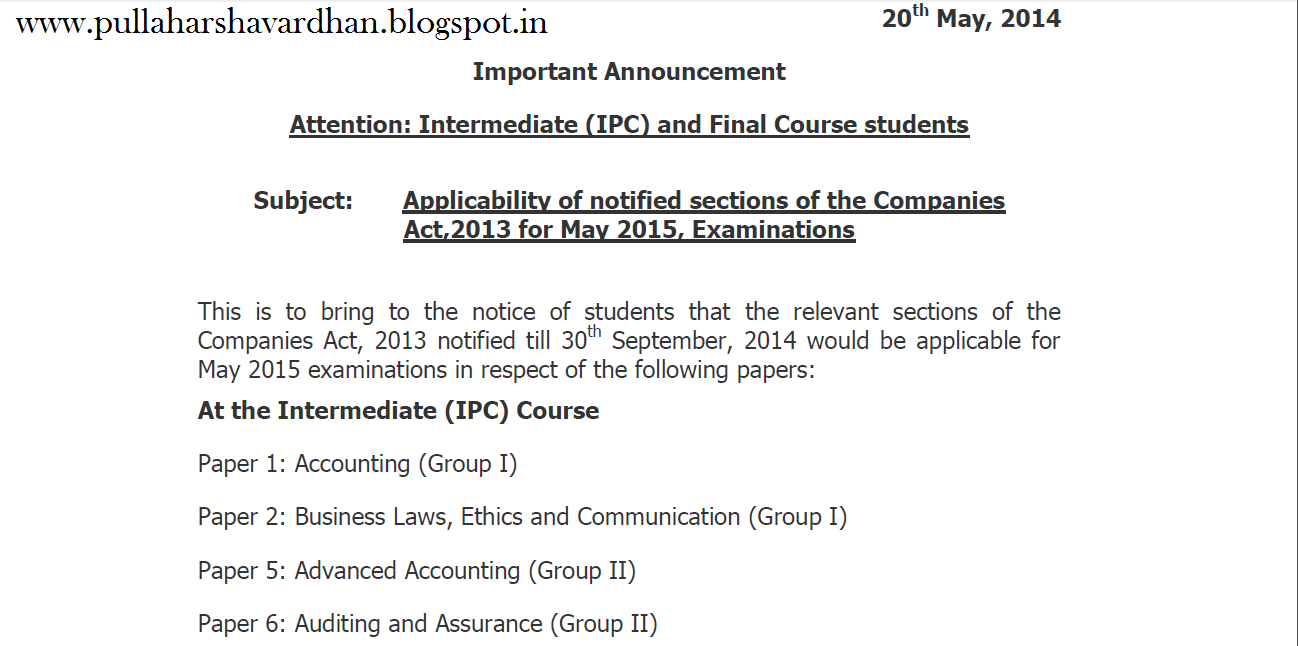

The Central Government has notified 98 sections of The Companies Act 2013 on 12th September, 2013. Accordingly, those 98 notified sections are applicable for November 2014 examinations corresponding to their bifurcation into the Intermediate (IPC) and Final Course(s),

i.e. from these 98 sections, 53 sections have been included in the Paper – 2, Business Laws, Ethics and Communication, Intermediate (IPC) Course, and 45 have been included in the Paper- 4, Corporate and Allied Laws, Final Course.

For Supplimentary Material of Law

Tuesday, 20 May 2014

Wednesday, 19 March 2014

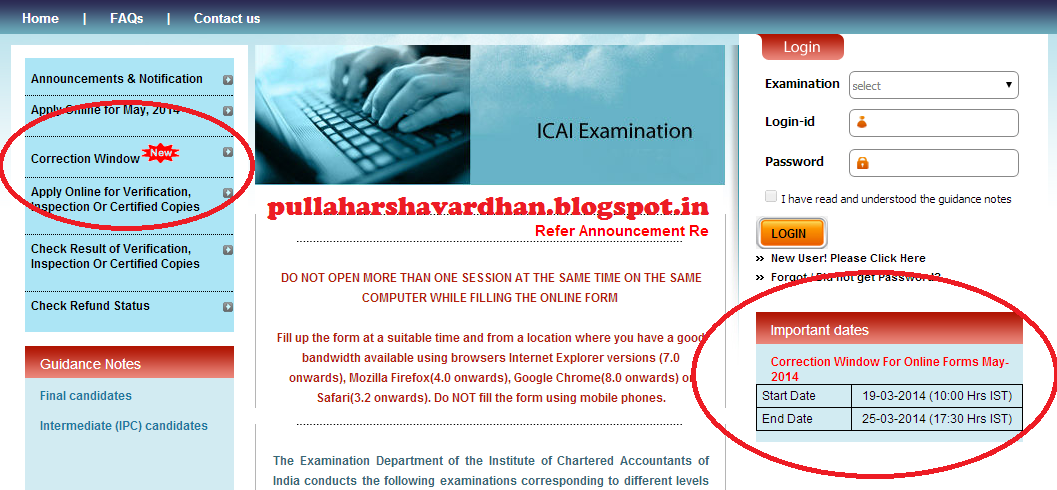

ICAI has brought in a " CORRECTION WINDOW "

Correction Window

“Correction Window” is a platform in the on line exam form submission process, where candidates can view and correct errors, if any, committed by them while submitting the exam form, in the fields, centre, group and medium opted. |

The terms and conditions in this regard are as follows: 1. This facility is available at http://icaiexam.icai.org, from 10.00 a.m. of 19.03.2014 to 5.30 p.m. of 25.03.2014 2. This facility is available only to those who had submitted their exam forms online. 3. This window is not for fresh submission of exam forms and is meant only for correction of errors if any, in the exam forms already submitted. 4. Candidates can access the portal by entering the following details, as filled in by them in their exam application forms: • Bar code number/control number printed on their online exam form • PIN ( i.e. the four digit number of their choice which they had filled in their exam forms) and • Date of birth. 5. Following details, submitted by the candidates in their online examination application form will be displayed on the screen. • Name of the candidate • Registration number and • Group/medium/centre opted 6. Candidates will be permitted to enter changes if any, in any of the following three fields only: • City opted. ( Change from domestic centre to abroad centre is not permitted) • Group opted ( Change from single group to both groups is not permitted) • Medium opted In other words, no fresh payment of exam fees or refund of exam fees already paid will be permitted on account of correction of groups, made in this process. 7. A change may include change of centre/group/medium either jointly or severally. 8. Candidate will not be permitted to make any corrections/changes to any other field. 9. The requests should be made by the student and not by anyone on his/her behalf. 10. Once you click “No change required”, no corrections can be submitted thereafter. So also, corrections, once submitted, cannot be changed thereafter. 11. The facility will be available free of cost. 12. The candidate should upload scanned copy of a handwritten application in this regard, duly signed by him, seeking the corrections required. Unless this condition is complied with, the candidate would not be able to submit corrections sought, online. 13. Those candidates ( who had submitted their exam forms online) and who might have already submitted a handwritten request for change of centre/group/medium, are advised to submit such request/s, online, through this Correction Window, once again. Changes sought through the Correction Window will be treated as final. 14. Admit cards will be issued based on the examination application form and the correction received till the Correction Window closes. 15. Those who had submitted physical OMR exam forms and seeking corrections in the fields mentioned above, may contact the exam department at: Final candidates: final_examhelpline@icai.in Indermediate (IPC) candidates: intermediate_examhelpline@icai.in Download the Full Notification |

Procedure To Use the “ Correction Window ”

Step 1 : Open www.icaiexam.icai.org and click on the Correction Window Option located at the left side

Step 2 : After reading the Instructions , Click on the Button “ I Have read And Understood the Above "

Step 3 : Fill All your Details as below and Click “ Login ”

.PNG)

Step 4 : All your Details will appear and To make changes Click On “ Change Required ”

.PNG)

Step 5 : Fill the Details which you want to change &

Click Submit .

Click Submit .

.PNG)

“Sharing IS Caring”

Sunday, 16 March 2014

Applicability of The Companies Act 2013 - November 2014 CA Exams

The Central Government has notified 98 sections of The Companies Act 2013 on 12th September, 2013. Accordingly, those 98 notified sections are applicable for November 2014 examinations corresponding to their bifurcation into the Intermediate (IPC) and Final Course(s), i.e. from these 98 sections, 53 sections have been included in the Paper – 2, Business Laws, Ethics and Communication, Intermediate (IPC) Course, and 45 have been included in the Paper- 4, Corporate and Allied Laws, Final Course.

For reference and benefit of our students, the Board of Studies has released the following publications relevant for November, 2014 examinations for Paper – 2, Business Laws, Ethics and Communication, Intermediate (IPC) Course, and Paper- 4, Corporate and Allied Laws, Final Course:

Supplementary study material for Intermediate (IPC) Course

Intermediate (IPC) Course

SYLLABUS

__________________________________________________

PAPER – 2 : BUSINESS LAWS, ETHICS AND COMMUNICATION

PART I – BUSINESS LAWS (60 MARKS)

Business Laws (30 Marks)

1. The Indian Contract Act, 18722. The Negotiable Instruments Act, 1881

3. The Payment of Bonus Act, 1965

4. The Employees’ Provident Fund and Miscellaneous Provisions Act, 1952

5. The Payment of Gratuity Act, 1972.

Company Law (30 Marks)

The Companies Act, 1956 – Sections 1 to 197

(a) Preliminary

(b) Board of Company Law Administration ─ National Company Law Tribunal; Appellate Tribunal

(c) Incorporation of Company and Matters Incidental thereto

(d) Prospectus and Allotment, and other matters relating to use of Shares or Debentures

(e) Share Capital and Debentures

(f) Registration of Charges

(g) Management and Administration – General Provisions – Registered office and name, Restrictions on commencement of business, Registers of members and debentures holders, Foreign registers of members or debenture holders, Annual returns, General provisions regarding registers and returns, Meetings and proceedings.

(i) Company Law in a computerized Environment – E-filing.

Note: If any provision of The Companies Act 2013 comes into force in place of an existing provision under the Companies Act, 1956 or otherwise by way of new provision, the syllabus would accordingly include the corresponding or new provisions of The Companies Act 2013, as the case may be.

Recommended Post

________________________________________________________________

Part II – : ETHICS (20 Marks)

1. Introduction to Business Ethics

The nature, purpose of ethics and morals for organizational interests; Ethics and Conflicts of Interests; Ethical and Social Implications of business policies and decisions; Corporate Social Responsibility; Ethical issues in Corporate Governance.

2. Environment issues

Protecting the Natural Environment – Prevention of Pollution and Depletion of Natural Resources; Conservation of Natural Resources.

3. Ethics in Workplace

Individual in the organisation, discrimination, harassment, gender equality.

4. Ethics in Marketing and Consumer Protection

Healthy competition and protecting consumer’s interest.

5. Ethics in Accounting and Finance

Importance, issues and common problems.

Part III – COMMUNICATION (20 Marks)

1. Elements of Communication

(a) Forms of Communication: Formal and Informal, Interdepartmental, Verbal and nonverbal;

Active listening and critical thinking

(b) Presentation skills including conducting meeting, press conference

(c) Planning and Composing Business messages

(d) Communication channels

(e) Communicating Corporate culture, change, innovative spirits

(f) Communication breakdowns

(g) Communication ethics

(h) Groups dynamics; handling group conflicts, consensus building; influencing and persuasion skills; Negotiating and bargaining

(i) Emotional intelligence – Emotional Quotient

(j) Soft skills – personality traits; Interpersonal skills ; leadership

2. Communication in Business Environment

(a) Business Meetings – Notice, Agenda, Minutes, Chairperson’s speech

(b) Press releases

(c) Corporate announcements by stock exchanges

(d) Reporting of proceedings of a meeting

3. Basic understanding of legal deeds and documents

(a) Partnership deed

(b) Power of Attorney

(c) Lease deed

(d) Affidavit

(e) Indemnity bond

(f) Gift deed

(g) Memorandum and articles of association of a company

(h) Annual Report of a company

SYLLABUS

PAPER – 6 : AUDITING AND ASSURANCE

________________________________________

1. Auditing Concepts ─ Nature and limitations of Auditing, Basic Principles governing an audit, Ethical principles and concept of Auditor’s Independence, Relationship of auditing with other disciplines.

2. Standards on Auditing and Guidance Notes ─ Overview, Standard-setting process, Role of International Auditing and Assurance Standards Board, Standards on Auditing issued by the ICAI; Guidance Note(s) on ─ Audit of Fixed Assets, Audit of Inventories, Audit of Investments, Audit of Debtors, Loans and Advances, Audit of Cash and Bank Balances, Audit of Miscellaneous Expenditure, Audit of Liabilities, Audit of Revenue, Audit of Expenses and provision for proposed dividends.

3. Auditing engagement ─ Audit planning, Audit programme, Control of quality of audit work ─ Delegation and supervision of audit work.

4. Documentation ─ Audit working papers, Audit files: Permanent and current audit files, Ownership and custody of working papers.

5. Audit evidence ─ Audit procedures for obtaining evidence, Sources of evidence, Reliability of audit evidence, Methods of obtaining audit evidence ─ Physical verification, Documentation, Direct confirmation, Re-computation, Analytical review techniques, Representation by management, Obtaining certificate.

6. Internal Control ─ Elements of internal control, Review and documentation, Evaluation of internal control system, Internal control questionnaire, Internal control check list, Tests of control, Application of concept of materiality and audit risk, Concept of internal audit.

7. Internal Control and Computerized Environment, Approaches to Auditing in Computerised Environment.

8. Auditing Sampling ─ Types of sampling, Test checking, Techniques of test checks.

9. Analytical review procedures.

10. Audit of payments ─ General considerations, Wages, Capital expenditure, Other payments and expenses, Petty cash payments, Bank payments, Bank reconciliation.

11. Audit of receipts ─ General considerations, Cash sales, Receipts from debtors, Other Receipts.

12. Audit of Purchases ─ Vouching cash and credit purchases, Forward purchases, Purchase returns, Allowance received from suppliers.

13. Audit of Sales ─ Vouching of cash and credit sales, Goods on consignment, Sale on approval basis, Sale under hire-purchase agreement, Returnable containers, Various types of allowances given to customers, Sale returns.

14. Audit of suppliers’ ledger and the debtors’ ledger ─ Self-balancing and the sectional balancing system, Total or control accounts, Confirmatory statements from credit customers and suppliers, Provision for bad and doubtful debts, Writing off of bad debts.

15. Audit of impersonal ledger ─ Capital expenditure, deferred revenue expenditure and revenue expenditure, Outstanding expenses and income, Repairs and renewals, Distinction between reserves and provisions, Implications of change in the basis of accounting.

16. Audit of assets and liabilities.

17. Company Audit ─ Audit of Shares, Qualifications and Disqualifications of Auditors, Appointment of auditors, Removal of auditors, Powers and duties of auditors, Branch audit , Joint audit , Special audit, Reporting requirements under the Companies Act, 1956.

18. Audit Report ─ Qualifications, Disclaimers, Adverse opinion, Disclosures, Reports and certificates.

19. Special points in audit of different types of undertakings, i.e., Educational institutions, Hotels, Clubs, Hospitals, Hire-purchase and leasing companies (excluding banks, electricity companies, cooperative societies, and insurance companies).

20. Features and basic principles of government audit, Local bodies and not-forprofit organizations, Comptroller and Auditor General and its constitutional role.

Note: If any provision of The Companies Act 2013 comes into force in place of an existing provision under the Companies Act, 1956 or otherwise by way of new provision, the syllabus would accordingly include the corresponding or new provisions of The Companies Act 2013, as the case may be.

Download | Notification

Subscribe to:

Posts (Atom)