Intermediate (IPC) Course

SYLLABUS

__________________________________________________

PAPER – 2 : BUSINESS LAWS, ETHICS AND COMMUNICATION

PART I – BUSINESS LAWS (60 MARKS)

Business Laws (30 Marks)

1. The Indian Contract Act, 18722. The Negotiable Instruments Act, 18813. The Payment of Bonus Act, 19654. The Employees’ Provident Fund and Miscellaneous Provisions Act, 19525. The Payment of Gratuity Act, 1972.Company Law (30 Marks)

The Companies Act, 1956 – Sections 1 to 197

(a) Preliminary

(b) Board of Company Law Administration ─ National Company Law Tribunal; Appellate Tribunal

(c) Incorporation of Company and Matters Incidental thereto

(d) Prospectus and Allotment, and other matters relating to use of Shares or Debentures

(e) Share Capital and Debentures

(f) Registration of Charges

(g) Management and Administration – General Provisions – Registered office and name, Restrictions on commencement of business, Registers of members and debentures holders, Foreign registers of members or debenture holders, Annual returns, General provisions regarding registers and returns, Meetings and proceedings.

(i) Company Law in a computerized Environment – E-filing.

Note: If any provision of The Companies Act 2013 comes into force in place of an existing provision under the Companies Act, 1956 or otherwise by way of new provision, the syllabus would accordingly include the corresponding or new provisions of The Companies Act 2013, as the case may be.

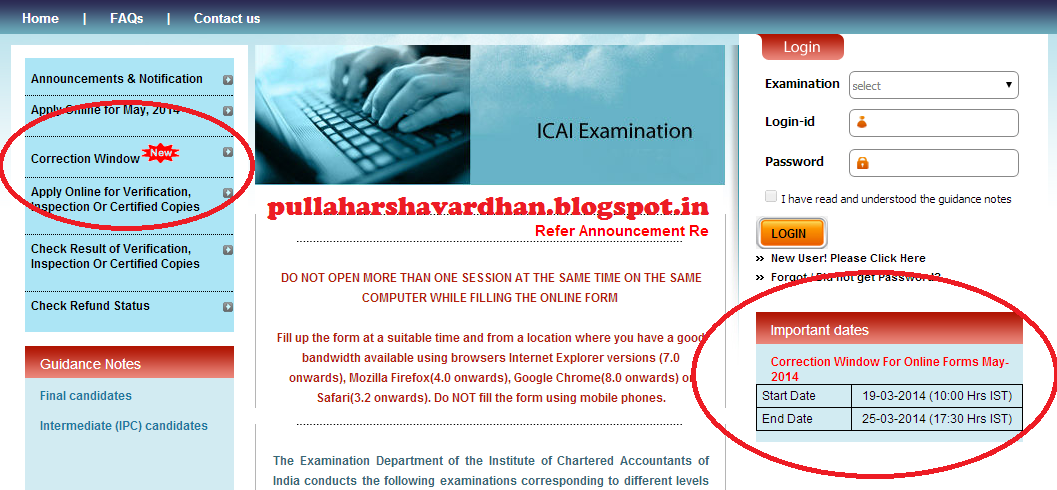

Recommended Post

________________________________________________________________

Part II – : ETHICS (20 Marks)

1. Introduction to Business Ethics

The nature, purpose of ethics and morals for organizational interests; Ethics and Conflicts of Interests; Ethical and Social Implications of business policies and decisions; Corporate Social Responsibility; Ethical issues in Corporate Governance.

2. Environment issues

Protecting the Natural Environment – Prevention of Pollution and Depletion of Natural Resources; Conservation of Natural Resources.

3. Ethics in Workplace

Individual in the organisation, discrimination, harassment, gender equality.

4. Ethics in Marketing and Consumer Protection

Healthy competition and protecting consumer’s interest.

5. Ethics in Accounting and Finance

Importance, issues and common problems.

Part III – COMMUNICATION (20 Marks)

1. Elements of Communication

(a) Forms of Communication: Formal and Informal, Interdepartmental, Verbal and nonverbal;

Active listening and critical thinking

(b) Presentation skills including conducting meeting, press conference

(c) Planning and Composing Business messages

(d) Communication channels

(e) Communicating Corporate culture, change, innovative spirits

(f) Communication breakdowns

(g) Communication ethics

(h) Groups dynamics; handling group conflicts, consensus building; influencing and persuasion skills; Negotiating and bargaining

(i) Emotional intelligence – Emotional Quotient

(j) Soft skills – personality traits; Interpersonal skills ; leadership

2. Communication in Business Environment

(a) Business Meetings – Notice, Agenda, Minutes, Chairperson’s speech

(b) Press releases

(c) Corporate announcements by stock exchanges

(d) Reporting of proceedings of a meeting

3. Basic understanding of legal deeds and documents

(a) Partnership deed

(b) Power of Attorney

(c) Lease deed

(d) Affidavit

(e) Indemnity bond

(f) Gift deed

(g) Memorandum and articles of association of a company

(h) Annual Report of a company

SYLLABUS

PAPER – 6 : AUDITING AND ASSURANCE

________________________________________

1. Auditing Concepts ─ Nature and limitations of Auditing, Basic Principles governing an audit, Ethical principles and concept of Auditor’s Independence, Relationship of auditing with other disciplines.

2. Standards on Auditing and Guidance Notes ─ Overview, Standard-setting process, Role of International Auditing and Assurance Standards Board, Standards on Auditing issued by the ICAI; Guidance Note(s) on ─ Audit of Fixed Assets, Audit of Inventories, Audit of Investments, Audit of Debtors, Loans and Advances, Audit of Cash and Bank Balances, Audit of Miscellaneous Expenditure, Audit of Liabilities, Audit of Revenue, Audit of Expenses and provision for proposed dividends.

3. Auditing engagement ─ Audit planning, Audit programme, Control of quality of audit work ─ Delegation and supervision of audit work.

4. Documentation ─ Audit working papers, Audit files: Permanent and current audit files, Ownership and custody of working papers.

5. Audit evidence ─ Audit procedures for obtaining evidence, Sources of evidence, Reliability of audit evidence, Methods of obtaining audit evidence ─ Physical verification, Documentation, Direct confirmation, Re-computation, Analytical review techniques, Representation by management, Obtaining certificate.

6. Internal Control ─ Elements of internal control, Review and documentation, Evaluation of internal control system, Internal control questionnaire, Internal control check list, Tests of control, Application of concept of materiality and audit risk, Concept of internal audit.

7. Internal Control and Computerized Environment, Approaches to Auditing in Computerised Environment.

8. Auditing Sampling ─ Types of sampling, Test checking, Techniques of test checks.

9. Analytical review procedures.

10. Audit of payments ─ General considerations, Wages, Capital expenditure, Other payments and expenses, Petty cash payments, Bank payments, Bank reconciliation.

11. Audit of receipts ─ General considerations, Cash sales, Receipts from debtors, Other Receipts.

12. Audit of Purchases ─ Vouching cash and credit purchases, Forward purchases, Purchase returns, Allowance received from suppliers.

13. Audit of Sales ─ Vouching of cash and credit sales, Goods on consignment, Sale on approval basis, Sale under hire-purchase agreement, Returnable containers, Various types of allowances given to customers, Sale returns.

14. Audit of suppliers’ ledger and the debtors’ ledger ─ Self-balancing and the sectional balancing system, Total or control accounts, Confirmatory statements from credit customers and suppliers, Provision for bad and doubtful debts, Writing off of bad debts.

15. Audit of impersonal ledger ─ Capital expenditure, deferred revenue expenditure and revenue expenditure, Outstanding expenses and income, Repairs and renewals, Distinction between reserves and provisions, Implications of change in the basis of accounting.

16. Audit of assets and liabilities.

17. Company Audit ─ Audit of Shares, Qualifications and Disqualifications of Auditors, Appointment of auditors, Removal of auditors, Powers and duties of auditors, Branch audit , Joint audit , Special audit, Reporting requirements under the Companies Act, 1956.

18. Audit Report ─ Qualifications, Disclaimers, Adverse opinion, Disclosures, Reports and certificates.

19. Special points in audit of different types of undertakings, i.e., Educational institutions, Hotels, Clubs, Hospitals, Hire-purchase and leasing companies (excluding banks, electricity companies, cooperative societies, and insurance companies).

20. Features and basic principles of government audit, Local bodies and not-forprofit organizations, Comptroller and Auditor General and its constitutional role.

Note: If any provision of The Companies Act 2013 comes into force in place of an existing provision under the Companies Act, 1956 or otherwise by way of new provision, the syllabus would accordingly include the corresponding or new provisions of The Companies Act 2013, as the case may be.

.PNG)

.PNG)

.PNG)